New Delhi, November 02, 2022, SIS Ltd. (NSE: SIS, BSE: 540673), announced its Unaudited Financial Results for the quarter that ended September 30th, 2022.

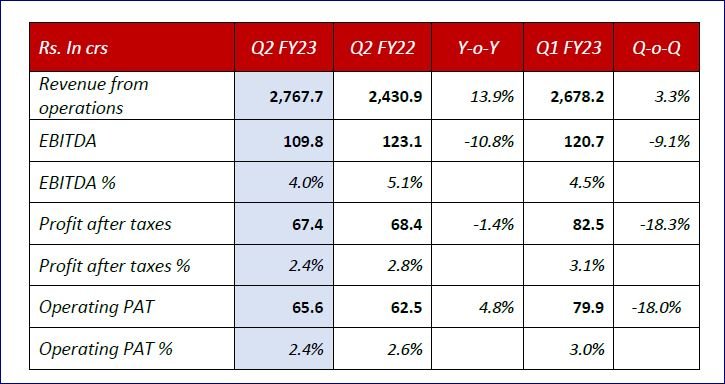

Key Consolidated Financials at a Glance:

Segmental Revenues are as follows:

- ‒ Security Solutions India: Rs. 1,150 Crs in Q2FY23 vs Rs 945 Crs in Q2FY22 and Rs. 1,058 Crs in Q1FY23

‒ Security Solutions International: Rs. 1,161 Crs in Q2FY23 vs Rs 1,156 Crs in Q2FY22 and Rs. 1,205 Crs in Q1FY23

‒ Facilities Management: Rs. 471 Crs in Q2FY23 vs Rs 336 Crs in Q2FY22 and Rs. 428 Crs in Q1FY23 - Return Ratios: RONW (based on proforma trailing 12 months PAT) is 18.0%, our strong return ratios continue.

- Cash Conversion – OCF/EBITDA on a consolidated basis was -27.8% for the quarter which is a direct result of the business growth and overall increase in DSO for the quarter. 8.8% Q-o-Q and 10.1% Q-o-Q revenue growth in Security Solution India and Facility management business respectively are the main drivers for decrease in OCF/EBITDA.

- Business Updates• India Security Solutions: The India security business continued the growth momentum with 8.8% QoQ and 21.7% YoY record organic growth in revenues and reached Rs. 1,150 Crs which is the highest in our history and clearly indicates that growth is back in India.

Major wins during the quarter came from Oil & Gas, Healthcare and Education segments. EBITDA margin for Q2 FY23 improved to 4.4% from 4.0% in Q1 FY23. - International Security Solutions: The International business recorded a revenue of Rs. 1,161 Crs which is a -3.6% QoQ decline and a 0.4% YoY increase over the same quarter in the previous year. After adjusting for the impact of temporary high margin covid related contracts reducing to a miniscule level in Q2 and special events revenue in Q1, the business grew 3.6% in constant currency on a normalized basis. As expected and indicated earlier, the EBITDA margins in Security Solutions – International business witnessed a decline in Q2 FY23, to 3.3%. This decline is a temporary phenomenon which is caused by a landmark wage increase in Australia. The closure of all COVID-related temporary high margin contracts also contributed to the decline in the EBITDA margins during the quarter. The gap caused by these timing differences is expected to be eliminated by Q3 FY23 and the full quarter effect will be visible in Q4 FY23.

- Facility Management Solutions: The Facility Management segment continued its strong recovery with revenue growth of 10.1% over Q1 FY23 and 40.1% over Q2 FY22, reaching revenues of Rs 471 Crs for the quarter. Major wins during the quarter came from Healthcare, Education, Commercial spaces and retail segments. The EBITDA margin was 4.4% in Q2 FY23, which is stable compared to 4.5% in Q1 FY23.

- Cash Logistics Solutions: The Cash Logistics segment continues its strong revenue growth with a revenue growth of 4.2% over previous quarter and 41.5% over Q2 FY22 driven by new wins in Door-step banking and Cash Processing Outsourcing business. The EBITDA margins also continue to improve and are a testament to the high margin nature of the cash logistics segment.

Commenting on the performance, Mr. Rituraj Kishore Sinha, Group Managing Director said, on the completion of 5 years since being listed, which included two difficult years impacted by the COVID-19 pandemic, we look back with a quiet sense of satisfaction of having built a highly stable and predictable business, resilient to economic variations, derisked from a geography and industry perspective, which consistently delivered revenue and business growth every year and continued distributions to shareholders in the form of dividends and buybacks every year.”